The Sequence of Returns Matters More Than You Think

- Jun 15, 2016

- 4 min read

For some, retirement can be stressful. The adjustment from a regular paycheck to living off your investments and Social Security can be scary. Plus, retiring confirms you are now officially old, which doesn't help. Seasoned investors have even more to worry about if they are unlucky enough to retire just prior to a market decline.

Investment volatility paired with systematic distributions can create a retirement shortfall for investors who suffer from poor (unlucky) timing. This portfolio danger is referred to as a Sequence of Returns risk. Surprisingly, the positive and negative annual returns early in retirement influence a portfolio's sustainability even more than the average return earned throughout retirement!*

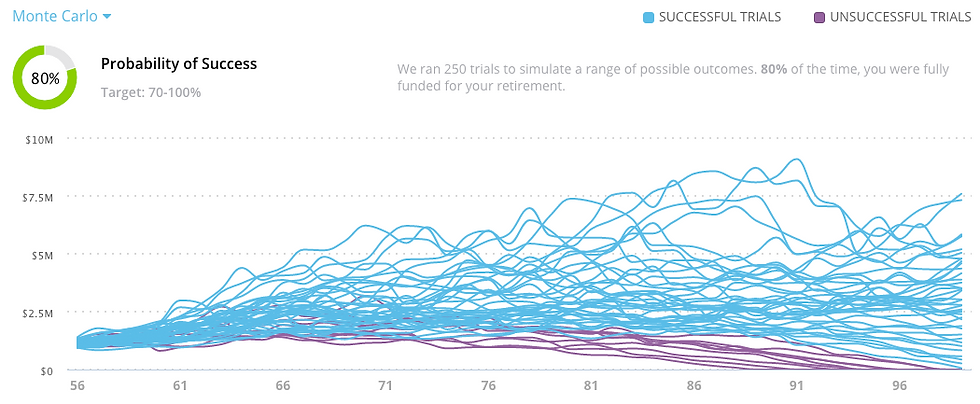

To illustrate the sequence of returns phenomenon, I modeled a 56 year old couple. They're currently funding retirement accounts, and plan to reduce expenses by 15% when they retire at age 67. Additionally, the couple plans to delay Social Security distributions until age 70. Statistically, things look pretty good at the moment.

Since you might be wondering, financial planners generally aim for success probabilities in excess of 75%. It's pretty difficult to get achieve a 100% success rate, but that's ok. Outcomes in the 75% - 85% range usually don't require huge spending adjustments in retirement, i.e., income adjustments are minor, and therefore quite palatable to most investors.

Let's assume these hypothetical investors retired in a "bad" year. When a one-year -10% market decline at age 66 is modeled, look what happens.

Their success rate dropped considerably, and this is only a -10% drop over a single year! Want to see what happens if we pretend it's 2008 (a -30% portfolio decline)?

That. Got. Ugly! So this couple is totally out of luck, right? It doesn't look promising, but let's look a little closer. The real story is that the returns achieved over the first DECADE of retirement matter more than the return achieved at retirement.** As long as an investor maintains a stock allocation (usually 40% to 60% is a valid target), they usually don't have to wait long for "better" returns to reappear. It's actually quite Rare an Investor Experiences an Entire Decade Without Positive Returns (at least it should be).

Since March of 2009, the stock market has gone on a fairly uninterrupted bull run. If you're within sniffing distance of retirement, you might be nervous a decline is right around the corner. Valid thinking or not, it could happen, so what should you do?

Here are six tactics you can take to mitigate an unfavorable sequence of returns if you turn out to be one of the unlucky.

Die Earlier. I know- it's not exactly good advice, but let's put the graphs above in perspective. The models I used rely on the couple living until age 100. Recently, the US Census Bureau estimated that only 0.0173% of the population will live that long. I know you're healthy, but statistically you're still not going to make it that long.

Adjust Expenses. Be flexible! In a bad market year, don't take the grandkids to Disneyland. Hunker down and wait out the market storm.

Limit Distributions To 4% Or Less. For years, a 4.5% portfolio withdrawal rate has been deemed safe. According to this month's Financial Advisor magazine, it still seems to be.

Take Social Security Earlier. During "normal" market conditions, a retiree can reasonably expect a higher overall income throughout retirement if benefits are delayed. However, if the market takes a drubbing at retirement, taking benefits earlier significantly reduces the strain on your portfolio. Even though your benefit amount is lower, taking the income early helps drive the overall retirement income success rate higher. If fact, when benefits are modeled for my hypothetical investors starting at age 67, their success rate jumps back up to 75% despite the -30% decline!

Execute Proper Account Spend Down. Run it like this: Required Minimum Distributions first (because you have to), cash flows from taxable accounts, then distributions from IRAs & Roth IRAs. The choice between the last two depends on prevailing tax brackets and their associated rates, and is easily a whole research paper in itself.

Liquidate Bonds During Declines. This strategy strays from conventional rebalancing and it requires an iron stomach. But, it allows for greater portfolio recovery. Since bonds typically hold up during market declines, selling your bond positions that haven't declined leaves 100% of the stock portion of the portfolio intact; primed to realize the entire breadth of gains during the ensuing recovery.

Working with an experienced financial planner who understands how to help investors navigate retirement surprises like Sequence of Returns risk is more valuable than you might think. In 2013, Morningstar Published A Study quantifying a good planner's additional value at 1.59%.***

For an investor with a $750,000 portfolio, that's an an extra $1,815,248 over 25 years (assuming a 7% return, no distributions, and annual compounding). My company, Aspen Leaf Partners, helps investors make these crucial planning decisions everyday. It's our focus, and we want you to benefit from our expertise.

A lot of times it's hard to know what you don't know. This is especially true with money. There's no harm in reaching out for an assessment of your personal situation. It's likely we'll be able to provide significant value over 1. continuing to do what you're used to doing, as well as 2. the financial salesperson at your local brokerage outlet. Don't be afraid to Shoot Us An Email in the footer below.

* Ready To Retire? When Planning for Income, Consider How the Sequence of Returns Could Impact a Portfolio’s Value Over Time. MFS Fund Distributors, Inc, January, 2016.

** Understanding Sequence Of Return Risk – Safe Withdrawal Rates, Bear Market Crashes, And Bad Decades. Nerd's Eye View Blog, Michael Kitces, October 1st, 2014.

*** Alpha, Beta, and Now... Gamma. Blachette & Kaplan, August, 2013.

Comments