Investment Performance: Luck or Skill?

- Apr 10, 2015

- 3 min read

The investment world has had a difficult time differentiating between luck or skill. In a January, 2015 InvestmentNews.com article, Meritt Finer writes that there's no clear method to evaluate luck vs. skill, at least in the investment niche of options trading. He does suggest that if a manager is analyzed over "a number of economic cycles" with "a large number of trades (hundreds)", their success means "we can be more confident that skill has played an increasingly greater role relative to luck.".

The author isn't necessarily talking about success in terms of outperformance, but rather profitability. The small difference is important. Almost every manager is profitable (how can they not be with the fees they normally charge!), but very few outperform. Finer's conclusion is that skill can be confirmed over the long term, with luck playing a role over shorter time frames.

The Academics Weigh In

In Fama & French's 2009 Journal of Finance paper Luck Versus Skill in the Cross Section of Mutual Fund Returns, the authors examined 3,156 actively managed funds from 1984-2006. Building upon previous work suggesting for every "good" manager there must be a "bad" manager on the other side of trade, the authors looked to test whether the good managers performance was due to luck or skill.

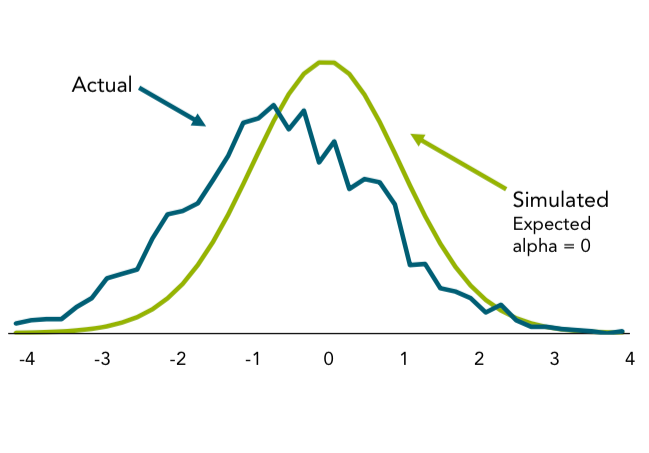

The authors first developed a sophisticated model simulation of expected performance, where half of the managers were expected to be good (above average performance) and half were expected to be bad (underperforming). In any scientific experiment, there must be a "control" to test a "variable" against. The expected returns simulation served as the control against actual manager performance, the variable.

What The Results Illustrate

Actual performance was lower than expected across the majority of the analysis. At every percentile below the 95th (statistically measured by t(α) intervals), less than 10% of the simulation runs produce a lower t(α) estimate than actual fund returns, which means more than 90% of the simulation runs beat the t(α) estimate for actual fund returns. In short, the simulations tell us that for the vast majority of actively managed funds, true α (alpha, our outperformance metric) is probably negative; that is, the fund managers do not have enough skill to produce risk adjusted expected returns that cover their costs.

Ok, Let's Not Get Too Dorked Up Here

The point of the the paper confirmed that a very small minority of fund managers did actually outperform due to skill, rather than luck. However, the next logical question we should ask is "Ok great, there do exist some talented managers. How can we identify them in advance?". That's a whole other hurdle to overcome for any investor trying to outperform the market!

Final Thoughts

With only a small minority of managers expected to outperform, trying to identify them and actually be invested in their strategies when they deliver above benchmark returns is statistically much riskier than rolling the dice in Vegas. While gambling should be viewed as entertainment where we should expect a cost (duh, gamblers usually lose), we shouldn't subject ourselves to even worse odds when investing.

The logical, sensible, Evidence-Based approach of buying market benchmarks via low cost index funds and ETFs should be the basis for any intelligent investment portfolio.

Next week we'll examine the ridiculous ways most investors (and in my opinion amateur financial advisors) choose investment strategies. Thanks for reading and putting up with my occasional grammatical errors. Have a great day!

Comments