Is It Safe To Ignore The Noise About Rising Interest Rates?

- Mar 24, 2015

- 4 min read

Yes, I'm still updating this blog. I try to post something relevant each week, but every once in a while I give myself a break. I'm sure my absence did everyone some good anyway :)

If you've read anything from the financial media in the last 3 years, you already know interest rates around the world are at historic lows. They can only go in one direction from here, right? The common wisdom says rising rates are really bad for bond investors. However, the truth may surprise you! This blog post will examine the historical results of interest rate increases, and how bond indices have actually performed.

Let's Start With Why Rates Are So Low

Central government banks in developed countries around the world have adopted the United State's strategy of injecting cash (via printing money and interest rate suppression) into the system to jump start their economies. Remember that Quantitative Easing thing I kept talking about in 2013 and 2014? Keeping rates low makes it easier for businesses to obtain cash to invest in development, and consumers typically buy more widgets when the cost of borrowed money is cheap. Both of these tactics tend to increase profits and stock valuations, signaling growth.

When Will Rates Rise?

When a government believes an economy is strong enough to withstand higher rates, they raise rates back up, usually in a series of intervals. In January, 2015, the FED updated its stance on raising rates. As a result, investors are either scrambling to re-arrange their portfolios, or sitting tight fearful to make an asset allocation change. The first type of investor is exhibiting irrational reactive behavior, and the latter is probably sweating it more than they should. The FED's intention is to raise short term rates this summer, no earlier than June. It's probable that rates won't move more than 0.5% in the first of what will probably be a series of increases.

Bond Interest Rate Sensitivity 201

The market values of bonds rise or fall depending on investors’ views about the outlook for inflation and interest rates, their perceptions about the creditworthiness of individual issuers, and their general appetite for risk. The yield on a bond is the inverse of its price. So if the price falls, it means investors are demanding an additional return, or "yield", on that bond to compensate for the risk of holding it to maturity. This sensitivity to interest rate change is called term risk. Financial advisors and investors have tried to mitigate this risk by reducing or eliminating intermediate and long duration bonds (those most sensitive to interest rate movements). Let's see if the odds have historically been on their sides.

What The Historical Data Shows

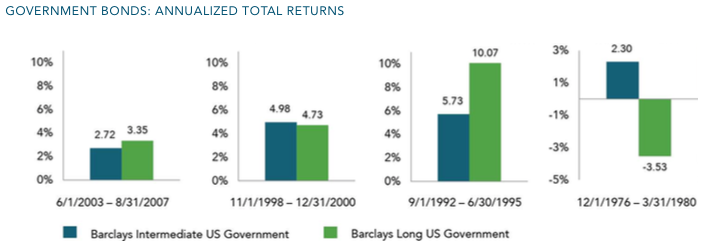

Using data going back to 1976, there have been 4 time periods lasting at least 12 months or more where the cummulative interest rate increase was at least 1.5 percentage points. The four periods were December 1976–March 1980 (when rates skyrocketed by 15.25 percentage points), September 1992–June 1995 (3 points), November 1998– December 2000 (1.75 points) and June 2003–August 2007 (4.25 points). The following chart illustrates how the very bonds folks are now reducing or eliminating have actually performed in the past.

Source: Barclays Capital data provided by Barclays Bank PLC via Dimensional Fund Advisors.

Within the time frame tested, only one bond asset class had a negative total return (total return includes bond interest plus share price appreciation / depreciation). That's an 87.5% success rate, and historically speaking, investors who are eliminating intermediate and long term bonds are probably screwing up!

There is validity in investment circles towards not using long term bonds in general. I personally haven't used them in years because I strongly believe bonds should represent safety in a diversified portfolio. The evidence shows long term bonds exhibit a higher degree of risk than than their short & intermediate counterparts. However, I disagree with investment professionals who omit long term bonds on the sole basis of trying to outguess the market, or in an attempt to protect against a future market event (which are extremely difficult to predict with accuracy and consistency). It's convenient marketing, but as history suggests, the strategy doesn't hold up well.

3 Reasons Why It's Safe To Avoid Interest Rate Noise

First, it's simply not true that bonds suffer when rates rise. In the short term, which I'll define as two years or less, bonds do quite well on average. Second, if rates rise, then the new bonds that are bought within your bond fund (or ETF) rise as well. This boosts the amount of dividends you receive from your fund, which of course you take as income (retirees), or reinvest if you don't need the money. Whichever camp you fall into, you benefit! Third, stocks have typically done well in rising rate environments. According to a January, 2015 Wall Street Journal article, "stocks have done well in past periods of rising interest rates, gaining an average of up to 8% or 10% annually". Even if bonds do suffer in the short term, chances are other parts of the portfolio will help prop it up.

Final Thoughts

The market is already anticipating that rates will rise. In other words, you can only benefit eliminating intermediate & long term bonds if interest rates actually rise faster and/or more than already expected. The worst thing you can do is buy into the media noise (or financial advice not grounded in science) and eliminate bonds. As my colleague Larry Swerdoe of Buckingham Asset Management put it: the surest way to win a loser’s game is to choose not to play.

Comments